Therefore, the business knows they need to keep fixed costs at £150,000 or under to attain their target profit. The business already knows their selling price is £150 per unit, their variable costs are £70 per unit and they expect to sell 5,000 units over the year. Suppose a business wants to know what their fixed costs should be, in order to hit a target profit of £250,000. The selling price needs to be increases from 15.00 to 16.13 in order to achieve the target profit of 15,000 with unit sales of 8,000. You use it by adding your desired profit to your fixed costs, then dividing that number by the price of each item minus its cost to make or buy.

Target Sales Volume Formula

Knowing this point helps managers make smarter decisions about inventory, staff levels, and other resources. Achieving target profit is a critical objective for businesses aiming to ensure long-term sustainability and growth. It involves not just setting financial goals but also implementing effective strategies and analysis techniques to meet these targets. The management sets budgets for sales and costs to achieve a target profit. Achieving profit requires controlling costs and achieving budgeted sales through this method.

Variables involved in the formula

Yes, it’s a good idea to use it often; this way, you stay on track with making as much money as you planned. Draw a line that represents the profit of P1 (the highest-ranked C/S product) scaled to the graph on the y-axis. Any adjustments for the variance in the actual and projected results can be adjusted in this final step as well. In previous pages of this chapter, we have focused mainly on the break-even point. However, the core objective of every business is not just to break even, but to earn a decent amount of profit.

Step 2: Calculate Total Revenue

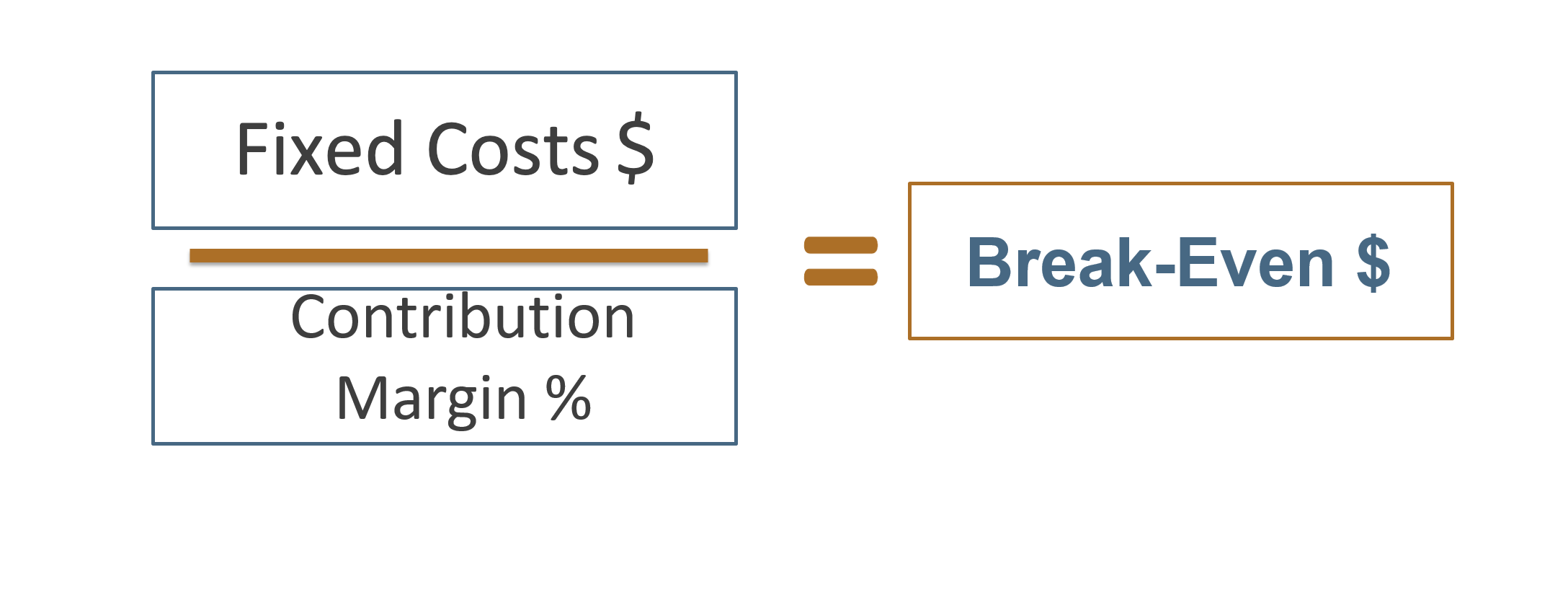

In all those cases, nonetheless, the CVP analysis can compute for the required sales volume. The CVP method finds the break-even sales point when the profit is set to zero. Instead of setting the profit to zero, the management can use the desired profit amount and follow the same steps to calculate the desired output quantity. If the profit is set to zero, the company can achieve the break-even point with the help of this equation. Else, the desired profit amount is set to determine the output quantity or the production volume level.

Managerial Accounting

An alternative method using the weighted average cost to sales (C/S) ratio can be used to determine the target profit as well. If the company ABC had set a target point, the crossing point at the x-axis will represent the required sales to achieve that target profit. The margin of safety in this problem is equal to target sales volume less break even sales volume.

- Additionally it decides that it can’t reduce the fixed costs or the production cost per unit, and needs to know the revised selling price to achieve the same target profit of 15,000.

- The target sales volume can be derived by tweaking the break-even formulae to incorporate the desired income.

- However, profit is often assumed to be the end result, a natural consequence of setting revenue and expense levels in the financial projections.

The management of a company named ABC Inc. after finalizing the target profit to be achieved in the next quarter wanted to equate the sales revenue that would be needed. For the evaluation of the revenue required following information is made available. By understanding the desired profit margin and considering the overall market, the business can lay the groundwork for sustainable growth.

Setting a target profit helps the management allocate resources efficiently. Now consider a business wants to know what their variance costs should be, in order to hit a target profit of £1.5m. It has fixed costs of £15,000 and each consultancy service delivered costs the business £1,000 each. Therefore, the business would need to sell 7,250 units to achieve their target profit.

One effective method for calculating target profit is the contribution margin approach. The contribution margin is the difference between sales revenue and variable 4 ways to protect your inheritance from taxes costs. By determining the contribution margin per unit, businesses can estimate how many units need to be sold to cover fixed costs and achieve the target profit.

Analyzing the sales mix involves examining the contribution margin of each product and understanding how shifts in sales volumes affect overall profitability. For example, if a company notices an increase in the sales of a high-margin product, it can expect an improvement in its overall profit margins. Conversely, a shift towards low-margin products might necessitate a reevaluation of pricing strategies or cost structures to maintain profitability. This analysis helps businesses make informed decisions about which products to promote or phase out. As an illustration, suppose the business estimates the market in the first year will be 8,000 units and is has the production capacity to accommodate this. Additionally it decides that it can’t reduce the fixed costs or the production cost per unit, and needs to know the revised selling price to achieve the same target profit of 15,000.

This method is particularly useful in scenarios where uncertainty is high, such as during economic downturns or when entering new markets. Aside from the determination of the break-even point, the CVP analysis can determine the level of sales required to generate a specific level of income. The target income could be expressed on a before-tax basis or after-tax basis.

The business already knows their selling price is £500 per unit, their fixed costs are £2.5m per year and they expect to sell 10,000 units over the year. Finally using the formula below the number of units it needs to sell to achieve the target profit level is as follows. Look at the past years’ financials to see patterns in costs and revenue. Allocate resources wisely, making sure they match up with expected revenues and desired profits. Sensitivity analysis is a powerful technique that allows businesses to understand how different variables impact their financial outcomes.

Recent Comments